Every Quote Is Free & Confidential

Every Quote Is Free & Confidential  Part and Part MortgageFlexible Part Repayment Options To Match your Budget. |

|

First Choice Finance have been established for over 30 years and we continue to arrange mortgages that are tailor made to suit our client`s requirements. This experience is just one reason that we are able to consider the option for part and part mortgages in line with the mortgage you are seeking. If you want the security of paying some of your mortgage balance off and the potential of still building on your equity, but wish to keep your monthly repayments to a minimum it could be worth getting a free quote on a part and part mortgage.

Our directly employed UK mortgage team can establish if you are eligible without obligation and provide you with a confidential free quotation, giving you all the facts and figures, for you to decide whether to proceed or not in your own time. Talk through your scenario on 0800 298 3000 (free phone) or dial 0333 003 1505 (mobile friendly), alternatively complete our shorton line enquiry form and we will call you. No credit search is carried out from this form.

Our directly employed UK mortgage team can establish if you are eligible without obligation and provide you with a confidential free quotation, giving you all the facts and figures, for you to decide whether to proceed or not in your own time. Talk through your scenario on 0800 298 3000 (free phone) or dial 0333 003 1505 (mobile friendly), alternatively complete our shorton line enquiry form and we will call you. No credit search is carried out from this form.What Is A Part and Part Mortgage?

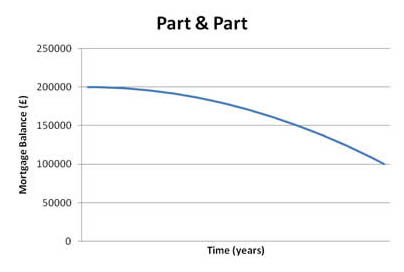

A part and part mortgage was designed to be the middle of the road when it comes to mortgage and remortgage repayment methods. It is rather simply just a combination of both an interest only mortgage and a repayment mortgage. You choose the amount of the initial loan or mortgage you would like to be on interest only and the remaining amount to be repaid entirely over the mortgage term as capital and repayment. Hence ``part`` of the balance is payable as interest only and therefore does not reduce and the other ``part`` is paid with both interest and capital each month to bring that part of the mortgage balance down. The idea behind it is that it incorporates the advantages of both capital and repayment and interest only repayment methods.

Hence ``part`` of the balance is payable as interest only and therefore does not reduce and the other ``part`` is paid with both interest and capital each month to bring that part of the mortgage balance down. The idea behind it is that it incorporates the advantages of both capital and repayment and interest only repayment methods. How Do Part and Part Mortgages Work?

Is It A Good Time To Look At A Part and Part Mortgage?

A part and part mortgage can be ideal in certain situations, especially when you are expecting some kind of windfall. Maybe you have an investment maturing or are expecting some inheritance or maybe even your work has got some sort of guaranteed long term bonus scheme in place. If you know that you have the means to pay off the capital part remaining on the interest only aspect of the part and part mortgage then these mortgage types can provide the perfect scenario to save on your monthly payments and still build equity in your property. If you are looking for flexibility a part and part mortgage can be the perfect remedy to combining the best of both worlds. You can choose the split between the repayment types. Not only that but you can sometimes amend the amounts when you wish to and are able to demonstrate you can afford the changes. Or if your financial situation changes, for example you come into some money earlier than expected or get a significant pay rise and would like to switch to a repayment mortgage to pay off the property in full by the end of the mortgage term, we can arrange that too (Subject to lending criteria).As with any mortgage you take out through ourselves you must seriously consider if it is the best option for your situation. Unfortunately part and part mortgages cannot erase all of the disadvantages involved when repaying a mortgage (as much as we would like them too!). Similar to an interest only mortgage, the part of your mortgage that hasn`t been paid off by the capital and repayment aspect will still be owed in full to the mortgage lender. It is your responsibility to ensure that you have a means to pay this outstanding debt at the end of the mortgage term, this element is often referred to as a repayment vehicle.

Part and Part Mortgages Compared To Other Repayment Options

When looking for a part and part mortgage it is essential to weigh up its pros and cons in relation to the other repayment options.Compared To A Repayment Mortgage

- Monthly repayments are cheaper on a part and part mortgage than for a comparable full repayment mortgage.

- You are paying interest on everything you owe but only part of the capital with a part and part repayment option.

- In the long run part and part is more expensive than full repayment.

- With a part and part mortgage you are left still owing the interest only ``part`` of the original mortgage advance to the lending company rather than owning the property outright with a repayment mortgage.

Compared To An Interest Only Mortgage

- Due to the capital and repayment element, monthly payments are higher with a part and part mortgage than a comparable interest only mortgage.

- Part and part mortgages are less expensive over the full mortgage term on a similar rate deal as you are paying off some of the capital.

- Unlike with an interest only mortgage with a part and part mortgage you will have built up some equity in your property due to the capital you have paid back over the term (subject to house price variations).

If you give us a call on 0800 298 3000 from a landline or 0333 0031505 from a mobile we can assess the advantages and disadvantages of all of the repayment options in regards to your situation in particular. If you want us to call you just fill in our no obligation short enquiry form and we will get right back to you.

How do part and part mortgages work

Video transcript

If you`re unsure about taking on a repayment mortgage or an interest-only mortgage, you may be interested to find out more about a part and part mortgage, which you could get through First Choice Finance.These kinds of deals fall in between the two traditional options, as they will let you pay off some of the capital on your property, but without requiring you to pay higher repayments each month to meet full capital clearance by the end of the term..

With a part and part mortgage, you can split the elements however you see fit, so if you`ve got a £150,000 deal, you could make capital and interest repayments on £100,000 of it and just pay the interest on the remaining £50,000, or you could split it down the middle and have £75,000 on each side.

Bear in mind that the larger the proportion that you leave as interest-only, the more you will have to pay back at the end of the mortgage term. Alternatively, if you pay back a greater amount of the capital over the course of the deal, you`ll have less to find at the end, but your repayments will have been higher.

Part and part mortgages can prove useful for people who plan to use investments to repay their home loan, but are aware these can come in lower than expected. This kind of deal can be used so that people can pay off much of their capital, but with lower repayments to help their cash flow through the mortgage term.

First Choice Finance can help you to find the most suitable part and part mortgage for you and all you need to do to get started is fill in our short application form on firstchoicefinance.co.uk. Alternatively, you can call 0800 298 3000 from a landline or 0333 003 1505 from a mobile to speak to our advisers.

Return to the video homepage

How Does A Part & Part Mortgage Work?What Does Capital And Interest Mortgage Mean?

What Mortgage Providers Offer Part & Part?

How Do You Calculate Payments On A Part & Part Mortgage?

What Happens To The Interest Only Element At The End Of The Mortgage Term?

How Does A Part & Part Mortgage Work?

Part and Part mortgages involve two different types of borrowing running at the same time and usually over the same term. In this case, of the total amount borrowed some of the mortgage is paid on an interest only basis and the remainder is paid on an interest and capital basis. This helps to keep payments lower during the mortgage term - however it is important to remember that the interest only component will still be owed at the end of the mortgage agreed term.

What Does Capital And Interest Mortgage Mean?

The standard way to repay a mortgage is to pay back an element of capital and the interest each month. At the beginning of the mortgage the interest is likely to be a larger element which reduces as the capital advanced at the outset becomes a smaller amount. At the end of an agreed term (usually 15 to 25 years) all of the required interest has been paid back and the initial amount taken will have reduced down to zero, so the mortgage is ended and no more money is due.

What Mortgage Providers Offer Part & Part?

Lenders tend to dip in and out of this style of lending so the only way to be sure is to talk to a mortgage adviser who has access to a wide selection of mortgage lenders. Some high street well known names may offer this but more will usually be available through specialist lenders who do not have a high street presence but obtain their clients through qualified approved mortgage advisers.

How Do You Calculate Payments On A Part & Part Mortgage?

There are specialised calculators to work this out or your mortgage adviser will demonstrate them to you. However you can work them out on a overall basis yourself. Just apply the rate on the interest only element to calculate the monthly interest due. This will be a flat payment throughout the term provided the rate does not change. For the Capital and Interest payment you can use a normal loan repayment calculator to get an idea of this element. Alternatively talk to a mortgage adviser.

What Happens To The Interest Only Element At The End Of The Mortgage Term?

Once you get to the end of the part and part mortgage the interest only element from the beginning will still be due. It will not have grown because you have been servicing the interest throughout, so that is some good news. However the lender will now want it`s money back. This is why it is important to have a repayment vehicle or other agreed route to settle this amount at the end of the term otherwise you can find yourself in a very tricky spot.

THINK CAREFULLY BEFORE SECURING OTHER DEBTS AGAINST YOUR HOME. |

Late repayment can cause you serious money problems. For help, go to moneyhelper.org.uk

Established In 1988. Company Registration Number 2316399. Authorised & Regulated By The Financial Conduct Authority (FCA). Firm Reference Number 302981. Mortgages & Homeowner Secured Loans Are Secured On Your Home. We Advice Upon & Arrange Mortgages & Loans. We Are Not A Lender.

First Choice Finance is a trading style of First Choice Funding Limited of 54, Wybersley Road, High Lane, Stockport, SK6 8HB. Copyright protected.